Key takeaways

- The balance sheet is a snapshot of what a UK business owns (assets), owes (liabilities), and has retained for shareholders (equity) at one specific date.

- The profit and loss statement measures income, expenses, and resulting profit over a period, usually the twelve-month financial year.

- Assets must equal liabilities plus equity on the balance sheet; this is the accounting equation that keeps double-entry bookkeeping internally consistent.

- Net profit from the P&L flows into the balance sheet through retained earnings, linking the two statements and maintaining the books in balance.

- Both statements are part of a UK limited company's statutory accounts filed annually with Companies House, and together they drive the corporation tax calculation on the CT600.

Balance Sheet vs Profit & Loss - Why They Matter

Managing a business isn’t just about chasing sales or closing deals, you’ve got to keep a close eye on your numbers. Financial statements are more than just paperwork for the taxman, they’re the backbone of smart decision-making. They show where your money is, how it’s moving, and whether you're driving your business in the right direction.

A lot of business owners stumble over the difference between a balance sheet vs profit and loss statement. Both are critical reports, but they don’t do the same job. The balance sheet gives you a snapshot of your company’s financial position at a specific moment. The profit and loss statement (P&L), on the other hand, is more of a play-by-play: it shows how much you’re earning, what you’re spending, and how those numbers shake out over time.

In this guide, we’ll break down what each statement means, how they differ, why you need both, and how to actually read them without needing a CPA on speed dial. By the time you’ve finished, you’ll have a clear view of what these reports show and how to use them to guide your business decisions with confidence.

What is a Balance Sheet?

Definition of a Balance Sheet

A Balance Sheet is an essential report of a company's financial position at a specific point in time, usually at the end of a fiscal quarter or year. Put simply, it’s a report that shows what your business owns, what it owes, and the value left for the owners at a specific point in time. Think of it as a financial snapshot, a quick picture of your company’s health on a given date.

For example, if your business owns £50,000 worth of assets but owes £20,000 in liabilities, the balance sheet will show an equity of £30,000. That £30,000 is the net worth of the business at that moment.

In practice, a balance sheet helps you see if your business is financially stable. A strong balance sheet could mean you’ve got robust cash reserves, manageable debts, and valuable assets. If liabilities are high or equity is shrinking, it’s a red flag that adjustments might be needed in how the business is run. In short, it’s a vital tool for making informed decisions and staying on top of your financial health.

The Balance Sheet follows the accounting equation: Assets = Liabilities + Equity.

The balance sheet is typically completed at the end of a month or a financial year. It is divided into two sections: the left side shows the assets of the company, while the right side shows the liabilities and shareholders' equity.

The total sum of all assets, less a business' total liabilities is equivalent to the owners' equity. This represents the amount that would be available for a business owner to draw out.

Components of a Balance Sheet

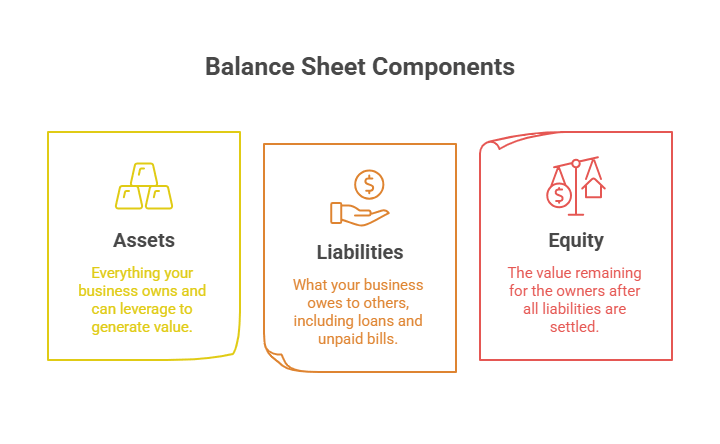

The balance sheet is built around three main parts:

1. Assets: This is everything your business owns and can leverage to generate value. Cash in the bank, inventory, equipment, property, outstanding invoices; if it’s valuable and belongs to the company, it goes here.

Current Assets: Current assets are essentially resources your company expects to either use up or turn into cash within a year (or within the normal operating cycle, whichever’s longer). These include cash on hand, accounts receivable, inventory, and prepaid expenses. They keep day-to-day operations running smoothly and make sure you’ve got the liquidity to cover short-term obligations as they come due.

Current assets are typically listed in the following order:

- Cash and cash equivalents - money immediately available for use.

- Marketable securities - investments like stocks and bonds you can quickly convert to cash

- Accounts receivable - outstanding payments owed by clients or customers.

- Inventory - goods available for sale or in production

- Prepaid expenses - Payments made in advance for items like rent, salaries, utility expenses and business insurance.

Non-Current Assets: Non-current assets, also known as long-term assets or fixed assets, are your long-term holdings. They’re expected to bring value to your business for more than a year. This category includes property, plant, equipment, intangible assets, long-term investments, and any receivables that aren’t due within the year. Non-current assets support your company’s strategic growth and operational stability.

Non-current assets are generally listed in the following order:

- Long-term investments - assets you intend to hold for more than a year like stocks, bonds, mutual funds, cash or real estate assets.

- Fixed assets - property or equipment that a company owns, and uses in its day-to-day operations for income generating activities like machinery, equipment, buildings and land.

- Intangible assets - non-physical assets such as goodwill, patents, copyrights, intellectual property, and customer lists. Note, intangibles are typically only recorded if acquired externally, not developed internally.

2. Liabilities: Here’s where you list what your business owes. Loans, unpaid bills to suppliers, taxes due, wages you haven’t paid out yet, if you owe it, it’s a liability.

Current Liabilities: Current liabilities are short-term obligations that a company expects to settle within a year or within its operating cycle, whichever is longer. We’re talking about things like accounts payable (money owed to vendors and suppliers), short-term loans, salaries you still need to pay, interest that’s due, dividends you’ve promised to shareholders, accrued expenses that have built up but haven’t been paid yet, and outstanding income taxes. You can pay current liabilities with current assets - cash on hand or assets you can quickly turn into cash.

Current liabilities include:

- Interest payable

- Salaries payable

- Accounts payable (your payables to suppliers/creditors)

- Dividends payable

- Accrued expenses (incurred costs not yet paid)

- Income taxes owed

Non-Current Liabilities: Non-current liabilities are the company’s long-term debts and commitments that extend beyond one year. This category includes long-term debt like bank loans and mortgages, bonds payable, capital leases, pension liabilities for future employee benefits, and customer deposits you’re holding onto for future services or products. These represent the company’s long term financial commitments which are essential for long-term planning and sustainability.

Long-term liabilities include:

- Long-term debt (loans, mortgages, debentures, etc.)

- Capital leases

- Bonds payable

- Pension liabilities

- Customer deposits

3. Equity: This is the value remaining for the owners after all liabilities are settled. Subtract what you owe (liabilities) from what you own (assets), and the remainder is equity - the owners’ stake in the business. Equity can be further divided into 3 components:

- Share capital: Owner's equity represents the funds initially invested by the company’s owners, also known as shareholders, and any additional capital shared into the business. It also includes retained earnings, which are the cumulative profits that the business chooses to reinvest for future growth instead of distributing as dividends.

- Retained Earnings: Retained earnings are the portion of net income that a company retains and reinvests in the business instead of distributing it to shareholders as dividends. It essentially function as the company’s internal reserve, used to support expansion, strengthen the balance sheet, or weather uncertain market conditions.

- Paid-In Capital: Also known as contributed capital, refers to the total amount investors provide in exchange for new shares issued by the company. This includes both the share capital and any surplus paid over the nominal share value. Together, these elements form the foundation of the company’s equity structure, supporting ongoing operations and future opportunities.

Why is a Balance Sheet Important?

A balance sheet isn’t just a string of figures, it’s your company’s financial status report card, front and center. By laying out exactly what your business owns and what it owes, it offers a real-time snapshot of your organisation’s value and stability.

Here’s why it’s important:

- Gives a clear view of financial health - The balance sheet gives you a straight answer about your financial health. Stronger assets than liabilities? You’re on solid ground. But if liabilities start overtaking assets, that’s a warning sign you can’t afford to ignore, it's time to investigate before issues snowball.

- Shows solvency - Comparing what you own with what you owe reveals whether your business can pay its bills as they fall due. A healthy balance sheet with stronger assets than liabilities signals good solvency and builds confidence with lenders or investors.

- Shows financial stability - When your assets look healthy and your debts are under control, it signals operational strength and resilience.

- Supports decision-making - When it comes to decision-making, a clear balance sheet is your best ally. You’ll know whether it’s smart to expand, hire, or pull back, based on actual numbers instead of guesswork.

- Helps with funding - Lenders and investors will absolutely demand your balance sheet. It’s a key document that shows if your business is worth their trust (and their money).

- Tracks growth - Compare balance sheets over time, and you’ll see whether your business is gaining value or slipping into more debt.

- Keeps you in control - It highlights warning signs like rising debt or low equity early, and you can address them before they escalate.

- Access to finance - When you’re seeking a loan, banks and lenders aren’t just handing out cash, they’re going to dig into your financials. Expect them to request your balance sheet, along with your profit and loss statement and cash flow report.

Balance Sheet Templates

Creating a balance sheet from scratch can feel a bit intimidating, especially if financial reports aren’t exactly your favorite thing. That’s where balance sheet templates come in handy. They’re basically a shortcut: just plug in your numbers and go. Saves you time and, honestly, a lot of hassle.

For small business owners, freelancers, or independent contractors, these templates are a game-changer. No need to be an accounting expert. Plus, when a bank, investor, or your accountant asks for reports, you’ll have your financials organised and ready to go.

Take a look at the sample balance sheet templates below. Use one to keep your business finances tidy, accurate, and always ready for review.

What is a Profit and Loss Statement?

Definition of a Profit and Loss Statement

A profit and loss statement, often called a P&L or income statement, is a financial report that tracks how much money your business has made and spent over a set period. It’s not the same as a balance sheet, which just shows your finances at one moment. The P&L actually paints the bigger picture, letting you see how your business is performing over weeks, months, or the whole year.

For example, say your business generates £80,000 worth of revenue during the year but spent £50,000 on wages, rent, and other costs. Your profit and loss statement would show a net profit of £30,000 for that period.

In practice, a P&L helps you see whether your business is operating profitably and where your money is going. It highlights if you’re making enough sales to cover your costs, whether expenses are rising too quickly, and how profitable your business really is.

Components of a Profit and Loss Statement

The profit and loss statement is built around three key parts:

1. Revenue (Sales)

Revenue is the total income a company earns from its primary business activities such as selling products or providing services. It’s the number at the top of the income statement, often called sales revenue. Basically, it’s the starting point before any expenses come into play.

2. Expenses

Expenses are basically the price of doing business, every pound a company has to shell out just to keep things running and pull in revenue. They are categorised into various types:

- Operating Expenses: These are expenses related to the day-to-day operations of the business, such as salaries, rent, utilities, marketing, and administrative costs.

- Cost of Goods Sold (COGS): COGS represents the direct costs of making whatever you’re selling. We’re talking raw materials, production labor, factory overhead - all the stuff that goes straight into your product.

- Other Expenses: These include non-operating expenses such as interest payments on loans, depreciation (the decrease in value of assets over time), and taxes. All the necessary evils that don’t fit neatly into the day-to-day operations.

3. Gross Profit and Net Profit

- Gross Profit: Gross profit is what’s left after you subtract the cost of goods sold (COGS) from your total revenue. Basically, it shows how much money you’re actually bringing in from your main business before you start paying for operating expenses, like salaries or rent. A solid gross profit margin usually means your production costs are under control, or your pricing strategy is on point; ideally both.

- Net Profit: Net profit, sometimes called net income or “the bottom line,” is the amount left over once all expenses have been paid. Net profit is a key indicator of whether the business is truly profitable after covering every single cost. If that number’s strong, you’re in a good spot. If not, you might need to take a closer look at where the money’s going.

Sample Profit Loss Statement

Why is a Profit & Loss Statement Important?

If you’re running a business, whether solo or with a team, P&L statement one of the most valuable reports for keeping track of day-to-day success.

- Measures Performance Over Time - The P&L shows you exactly what’s coming in and what’s going out, week by week or month by month. You’ll see patterns right away, like steady growth or warning signs if costs start eating up your profits. Without it, you’re basically guessing at how well you’re doing.

- Helps Control Costs - It breaks down your expenses into clear categories like rent, payroll, supplies, and makes it easy to spot waste, cut unnecessary costs, and keep more money in the business. Nobody likes seeing their hard-earned cash disappear on stuff that doesn’t move the needle.

- Supports Better Decision-Making - With real numbers in front of you, you can make smarter moves - whether it’s pricing, new hires, investments, or expansion. If profits are dipping, that big spend can probably wait. The P&L keeps you grounded in reality.

- Simplifies Tax and Compliance - When tax season arrives, your P&L saves the day. It makes calculating taxable income straightforward, keeps you compliant, and takes a lot of stress out of year-end reporting. No more scrambling for receipts or digging through spreadsheets.

- Builds Credibility with Lenders and Investors - Banks and investors almost always want to see your P&L before they offer loans or funding. A solid statement with consistent profits makes you look professional and reliable, two things that open doors.

- Keeps You Focused on Growth - The P&L doesn’t lie. Review it regularly and you’ll stay focused on what actually drives growth, instead of relying on gut instinct. It’s your reality check and your roadmap.

P&L Templates

A Profit & Loss (P&L) statement is a key tool for tracking how well your business is performing. But creating one from scratch isn’t always easy, especially if you’re busy running day-to-day operations. That’s where ready-to-use P&L templates can help. They give you a simple structure to record income, expenses, and profits, so you spend less time formatting and more time understanding your numbers.

To make things easier, we’ve put together some sample P&L templates to make it easier for you to get started.

Difference Between Balance Sheet and Profit and Loss Statement

The balance sheet gives you a clear-cut snapshot of your business’s financial position right now - assets, liabilities. Think of it as a status report for where the company stands today. On the flip side, the profit and loss statement tracks your business’s performance over a set period. It lays out how much money you brought in, what you spent, and what’s left over.

The balance sheet tells you what you’ve got and what you owe at this moment, while the P&L breaks down how you actually got here; through sales, expenses, and everything in between.

When you use both together, you get the full financial picture: not just where your business stands at a single moment, but also how well you’ve been doing over time.

Here’s a quick rundown of their main differences:

Here’s how it works in the business world:

A balance sheet gives you a clear picture of what your company owns and owes at a specific moment. It’s something banks look at closely when you’re seeking a loan, since strong assets and manageable debts make your business look like a safe bet.

Then you’ve got the profit and loss statement. On the surface, sales might seem solid, but if expenses are rising, profits can take a hit and that’s a red flag for cost control.

To sum it up, the balance sheet shows where your business stands right now; the profit and loss statement shows the journey that got you there. Both are valuable on their own, but when you review them together, you get the complete financial picture of your business.

How Balance Sheet and P&L Work Together

A balance sheet and a profit and loss statement are built differently, but they’re basically two sides of the same coin. Looking at just one? You’re only getting part of the story. Together, they actually show you what’s going on with your company’s finances.

The profit and loss statement (P&L) tells you if you’re making money over a certain period i.e are you profitable or not? But the balance sheet? That’s where you see what you actually own, what you owe, and whether your business is financially stable at this moment. Sometimes, you’ll see great profits on the P&L, but then the balance sheet drops a reality check; maybe cash is running low, or debts are higher than you’d know. So, on paper, things look good, but in practice, you might be struggling to pay bills or cover payroll.

For small businesses and contractors, it’s critical to review both reports together. Let’s say you’re a contractor. Your P&L shows steady profits, but look closer at the balance sheet and maybe you’ll see a pile of unpaid invoices, and suddenly, you realise your cash flow’s tighter than you thought. If you skip checking both, you could miss risks that sneak up on you.

In short, the balance sheet is your snapshot of financial stability, and the P&L shows your performance over time. Use them together, and you’ll be able to spot risks, find growth opportunities, and make better strategic decisions with a lot more confidence.

Balance Sheet and P&L: The Duo Every Business Needs

The balance sheet and the profit and loss statement work hand in hand. The balance sheet shows you where your finances stand right now, while the profit and loss statement tracks how you’ve actually been performing over time. Keeping tabs on both means no nasty surprises and helps you grow your business in the right direction.

For small businesses, contractors, and freelancers, these reports aren’t just helpful but essential. They keep you in control, support better tax planning, and help you make smarter choices for the future.

If you’d like expert help with your balance sheet, profit and loss statement, GoForma is here to make things simple. With professional support by our small business accountants, you can maintain accurate records, interpret financial data effectively, and optimise financial strategies for growth.

Book a free consultation today and see how GoForma can make your finances simpler.