Key takeaways

- A P11D reports taxable benefits in kind provided to UK directors and employees, such as company cars, private medical insurance, and interest-free loans over £10,000.

- The P11D filing deadline is 6 July after the end of the tax year the benefits relate to, with Class 1A National Insurance due on the P11D(b) by 22 July if paid electronically.

- Class 1A National Insurance on benefits in kind is charged at 15% from 6 April 2025, up from 13.8%, matching the increased employer Class 1 rate.

- Benefits reported on payroll under the optional payrolling of benefits scheme do not need to appear on a P11D, but the P11D(b) declaration of Class 1A NIC is still required.

- HMRC charges £100 per 50 employees per month for late P11D filing, and 5% of the Class 1A NIC plus interest for late payment of the liability.

What is P11D?

The P11D is the official HMRC form reference (Form P11D - Expenses and Benefits) used to declare the cash value of benefits in kind provided by UK employers to their workforce. It records employment benefits that the employees and directors of a company have received across the year.

P11D form is a declaration that employers must submit to HMRC annually. It reports the value of any benefits and expenses provided to employees that aren't included in their salary. These benefits might include things like company cars, private health insurance, and interest-free loans.

Each P11D form includes your basic identifying information, along with various sections that cover a range of benefits and expenses-from accommodation, to vouchers, credit cards and mileage allowance.

Accurate completion of the P11D form is essential to calculate the correct tax liability for both employers and employees. It must be filed by July 6th of each tax year and is a crucial part of payroll and tax returns. Employers can submit the P11D form online through HMRC's PAYE online service or utilising third-party software.

Who Must File a P11D?

UK employers must file individual P11D forms for:

- All company directors (regardless of earnings)

- Employees receiving taxable benefits beyond their regular salary

- Part-time and temporary staff who receive benefits

- Sole directors of limited companies (acting as both employer and employee)

Exception: Sole traders and partnerships without employees don't need to file P11D forms, as expenses are reported through self-assessment tax returns instead.

What Benefits Must Be Reported on P11D?

The P11D form is the go-to document for reporting "benefits in kind," which are essentially the extra benefits employees get on top of their salary.

The information typically includes details about expenses or benefits such as:

Vehicle Benefits:

- Company cars and fuel

- Car parking spaces

- Company vans for personal use

Insurance and Healthcare:

- Private medical insurance

- Health screenings and gym memberships

- Life insurance policies

Financial Benefits:

- Interest-free or low-interest loans over £10,000

- Credit cards for personal expenses

- Cash vouchers and non-cash vouchers

Property and Assets:

- Living accommodation provided by employer

- Use of company assets (phones, computers for personal use)

- Assets transferred to employees

Other Perks:

- Non-business travel and entertainment

- Professional subscriptions paid by employer

- Childcare vouchers (in some cases)

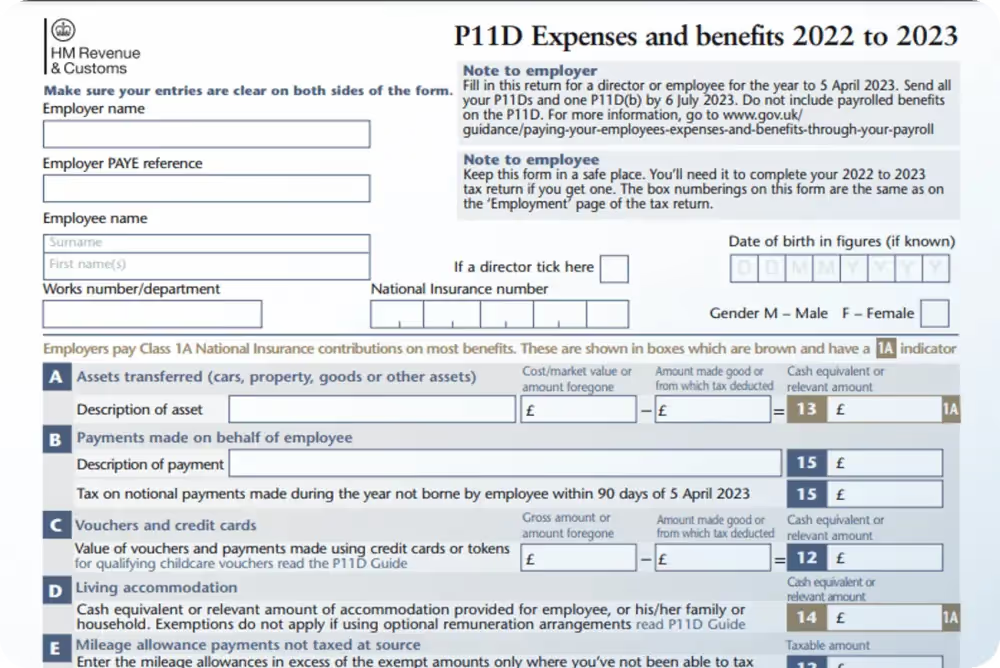

Sample P11D Form

Below is the sample of how P11D form looks like:

What NOT to Include on P11D

Since April 2016, genuine business expenses are exempt from P11D reporting. These include:

- Business travel and accommodation

- Business entertainment expenses

- Professional fees and subscriptions (required for work)

- Work uniforms and tools

- Mobile phone bills (for work purposes)

- Mileage allowance at HMRC-approved rates

How to Submit P11D Forms

Employers can file P11D forms through:

- HMRC PAYE Online Service (for businesses with up to 500 employees)

- Compatible payroll software (automatic filing)

- Third-party payroll providers (outsourced submission)

P11D Deadline

The P11D form must be submitted by July 6th each tax year to avoid penalties. For the tax year 2025/26, the P11D deadline is July 6, 2026. This deadline covers benefits and expenses provided to employees during the previous tax year, which runs from April 6th to April 5th. The submission can be done online, or using third-party payroll software. It serves as the basis for payrolling benefits or filing the P11D(b) form.

P11D Late Filing Penalties

- If you submit your P11D form late, there’s a penalty of £100 for every 50 employees for each full month it’s overdue.

- For late National Insurance Contributions (NICs), a 5% penalty applies if payment is more than 30 days late. This penalty rises to 10% after 6 months and goes up to 15% after 12 months, with interest charged on the outstanding amount.

Penalties can also be issued if inaccurate information is provided on your tax return, whether due to carelessness or deliberate action. This may result in:

- underpaying taxes

- over-claiming tax reliefs

P11D(b) Form: The Companion Declaration

What is P11D(b) Form?

The P11D(b) form accompanies your P11D submissions and calculates the total Class 1A National Insurance Contributions due on all employee benefits provided throughout the tax year.

When You Must Submit P11D(b):

- You've submitted any P11D forms

- You've payrolled employee benefits and expenses

- HMRC has specifically requested it

One P11D(b) covers your entire company, summarising all benefits across all employees, whereas individual P11D forms are needed for each employee.

Do I Need to Give Employees a Copy of Their P11D?

Yes, by law, employers must provide each employee with a copy of their P11D form by July 6th. Employees need this information to:

- Complete their self-assessment tax return accurately

- Verify the benefits reported match what they received

- Request corrections if information is inaccurate

- Claim tax repayments if applicable

Employees can also request copies directly from HMRC if their employer doesn't provide them.

Alternatives to P11D Filing

Payrolling Benefits

Instead of filing P11D forms annually, employers can payroll benefits by:

- Registering benefits with HMRC before April 6 (start of tax year)

- Including benefit values in employees' regular payroll

- Deducting tax monthly through PAYE system

- Providing benefits statements to employees by June 1

Important: Even when payrolling benefits, you still must submit P11D(b) to report Class 1A NICs.

PAYE Settlement Agreements (PSAs)

For minor, irregular, or impractical benefits, employers can arrange a PSA with HMRC to:

- Make one annual payment covering all tax and NICs

- Avoid processing items through payroll

- Skip P11D forms for covered items

- Pay Class 1B (not 1A) National Insurance instead

Suitable for: Small gifts, staff entertaining, shared company assets.

Differences Between P11D and P11D(b) Forms

The main difference between the P11D and P11D(b) forms is their purpose. The P11D form is used to report employee benefits, while the P11D(b) form is used to account for tax. Additionally, the filing deadline for both forms is July 6th. The P11D form is necessary when benefits are not payrolled, whereas the P11D(b) form is required when benefits are payrolled. Furthermore, the P11D form is employee-specific, while the P11D(b) form is company-wide.

Get Help with Your P11D Forms

When to Seek Professional Advice:

- First-time employers unsure what to report

- Complex benefit calculations (company cars, living accommodation)

- Multiple employees with varied benefits

- Previous filing errors needing correction

- Considering switching to payrolling benefits

GoForma's small business accountants can help with P11D preparation, submission, and ongoing compliance, ensuring you meet all deadlines and avoid penalties.