Key takeaways

- A VAT return is a quarterly submission to HMRC that reports VAT charged on sales (output tax) minus VAT paid on purchases (input tax) to calculate the net amount owed or reclaimable.

- The standard VAT return contains nine boxes covering output VAT, input VAT, net VAT due or refundable, total sales and purchases excluding VAT, and EU goods trade values.

- Quarterly VAT return deadlines fall one month and seven days after the end of each accounting period, and late submissions trigger penalty points under the new HMRC points-based regime.

- Businesses must register for VAT when taxable turnover exceeds £90,000 in any rolling 12-month period, though voluntary registration below this threshold is allowed.

- Alternative schemes such as the Flat Rate Scheme, Annual Accounting Scheme and Cash Accounting Scheme change how often you file or how you calculate VAT on your returns.

VAT Returns Explained

VAT is a consumption tax placed on goods and services at each stage of production or distribution. It’s ultimately paid by the end consumer, but businesses collect and remit it to HMRC.

VAT returns are the regular reports businesses submit to HMRC detailing the VAT they’ve charged on sales (output tax) and the VAT they’ve paid on purchases (input tax). These returns help ensure that the correct amount of VAT is collected and paid to the government. Every business that is registered for VAT must submit a VAT Return to HMRC on a regular basis.

What is a VAT Return?

A VAT return is a document that businesses in the UK submit to HMRC to report the amount of VAT they have charged on their sales (output tax) and the amount of VAT they have paid on their purchases (input tax). It details the amount of VAT that a business has collected and paid during a specific period of time. This period of time is usually a quarter, although some businesses may be required to submit a return more frequently. This return helps HMRC ensure that businesses are paying the correct amount of VAT and allows businesses to reclaim any VAT they have paid on business expenses. The VAT Return must be completed accurately and submitted to HMRC by the due date in order for the business to remain compliant with the law.

Components of a VAT Return

Understanding the key components of a VAT Return is essential for accurate and compliant reporting.

Sales and Purchases

- Sales (Output Tax): This section includes all sales and income on which you’ve charged VAT. It covers the total value of goods and services sold, both to customers within the UK and internationally, if applicable.

- Purchases (Input Tax): This section includes all business-related purchases and expenses on which you’ve paid VAT. It includes raw materials, stock, equipment, and other business expenses that are subject to VAT.

Calculating VAT Due to HMRC

Once you’ve listed your sales and purchases, you need to calculate the VAT due to HMRC. This involves a few key steps:

- Total Output Tax: Add up the VAT you’ve charged on your sales. This is your output tax.

- Total Input Tax: Add up the VAT you’ve paid on your purchases. This is your input tax.

- Net VAT Due: Subtract the total input tax from the total output tax. If your output tax is greater than your input tax, you owe the difference to HMRC. If your input tax is greater than your output tax, you can reclaim the difference from HMRC.

VAT Return Example

Let’s put it all together with a practical example. Suppose your business has the following transactions in a quarter:

- Sales: £10,000 (with 20% VAT)

- Purchases: £4,000 (with 20% VAT)

Output Tax Calculation

- Total sales: £10,000

- Output tax: £10,000 x 0.20 = £2,000

Input Tax Calculation

- Total purchases: £4,000

- Input tax: £4,000 x 0.20 = £800

Net VAT Calculation

- Output tax: £2,000

- Input tax: £800

- Net VAT: £2,000 - £800 = £1,200

In this example, you owe HMRC £1,200.

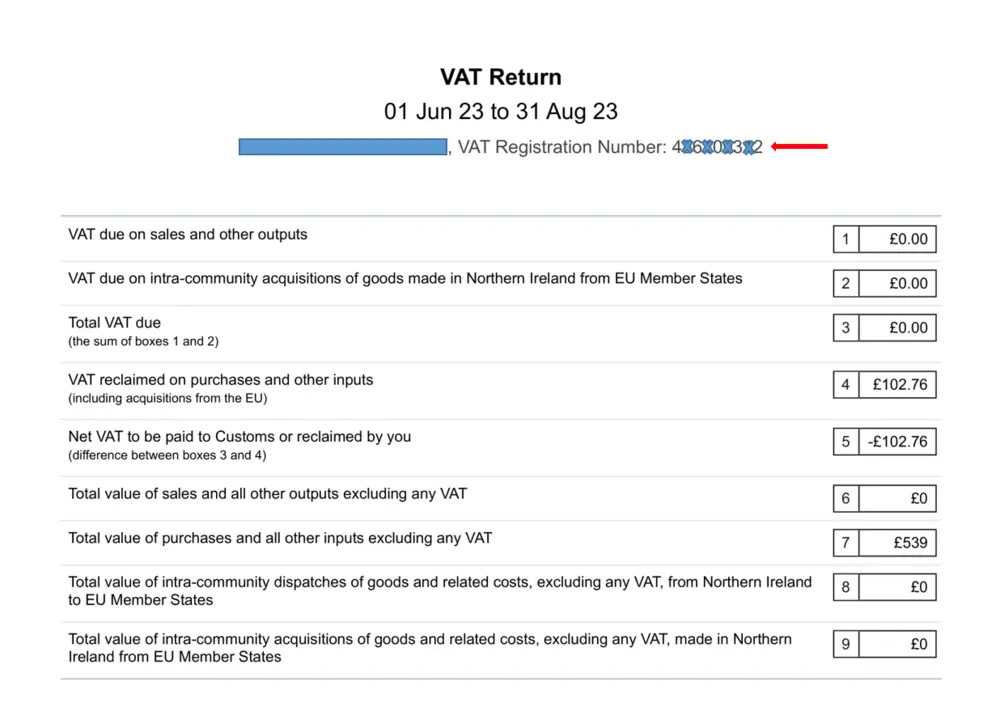

Sample VAT Return

Here are the components of a sample VAT return form used by businesses to report their VAT transactions to HMRC.

Who Needs to Submit VAT Returns?

Submitting VAT Returns is a crucial task for VAT registered businesses in the UK. To understand who needs to submit these returns, we need to look at mandatory VAT registration and the potential benefits of voluntary VAT registration.

Mandatory VAT Registration

Businesses must register for VAT if their taxable turnover exceeds the VAT threshold. As of the 2024/25 tax year, the VAT threshold is £90,000 in a 12-month period.

Voluntary VAT Registration

Even if your business doesn’t meet the mandatory registration criteria, you can still choose to register for VAT voluntarily. This can be beneficial in several ways:

- Reclaiming VAT on Purchases: By registering for VAT, you can reclaim the VAT you pay on business-related purchases, which can be significant if you incur a lot of VAT on expenses.

- Improved Business Image: Being VAT-registered can enhance your business’s credibility and professionalism, particularly if your clients and competitors are also VAT-registered.

- Cash Flow Management: Voluntary registration allows you to manage your cash flow more effectively by reclaiming VAT on purchases, which might be useful for startups or small businesses with high initial costs.

- Expanding Business: If you plan to expand your business and expect to surpass the VAT threshold soon, registering early can help you avoid the rush and ensure compliance from the outset.

Calculating VAT

Calculating VAT correctly is important for businesses to meet tax obligations. Use our VAT calculator to simplify calculations. Just enter the total amount of goods or services, choose the VAT rate (like standard 20% or reduced rates), and the calculator will quickly show you the VAT amount. This tool helps ensure accurate VAT calculations, making it easier to comply with HMRC regulations.

How to File Your VAT Return

Filing your VAT return doesn't have to be complicated. HMRC provides several methods to make the process straightforward, especially with Making Tax Digital (MTD) in place.

- Accounting Software: Use MTD compatible software to submit your VAT return directly through it.

- Accountant: You can appoint a small business accountant to handle your VAT return for you. They'll ensure everything is submitted correctly.

- VAT Online Account (for Annual Accounting Scheme users): If you're part of the VAT Annual Accounting Scheme, you can submit your return through your VAT online account.

- By Post (in special cases): If you're exempt from Making Tax Digital for VAT, you can submit your return by post or another approved method.

Pay Your VAT Bill

Here's how you can pay your VAT bill:

- Pay Electronically: Use Direct Debit, debit or corporate credit card, or internet banking to make your payment securely to HMRC online.

- Get Payment Confirmation: When using the online service, HMRC will provide you with a payment reference number instantly.

- Check Payment Status: You do not need to contact HMRC to confirm receipt of your payment. Instead, check your VAT online account within 3 to 5 days after payment. This is where your payment status will be updated.

Remember, if you're unable to pay your VAT bill, Contact HMRC to discuss your options.

VAT Return Deadlines

The frequency of filing VAT returns depends on the scheme your business is registered under. The most common is the quarterly return, but there are also annual accounting and other special schemes.

Quarterly Returns

Most businesses file their VAT returns quarterly. This means you will submit a VAT return every three months. Each quarter, you will need to calculate your total sales, purchases, output tax, and input tax, then report these figures to HMRC. The deadlines for submitting quarterly returns and paying any VAT owed are usually one month and seven days after the end of the accounting period.

Businesses are assigned specific quarters by HMRC, which typically follow the calendar year. For example, if your VAT quarters are aligned with the calendar year, your deadlines might look like this:

- 1st Quarter (January to March): Return due by April 7th

- 2nd Quarter (April to June): Return due by July 7th

- 3rd Quarter (July to September): Return due by October 7th

- 4th Quarter (October to December): Return due by January 7th

Annual Accounting Scheme

The annual accounting scheme allows businesses to file one VAT return per year instead of four. This can simplify the process and reduce the administrative burden, especially for small businesses. Under this scheme, businesses make advance VAT payments throughout the year based on an estimate of their total VAT liability. At the end of the year, they submit a single VAT return and either make a final payment or receive a refund if they have overpaid.

Key Points:

- Eligibility: To qualify for the annual accounting scheme, your estimated taxable turnover must be £1.35 million or less.

- Payments: You make nine monthly or three quarterly interim payments throughout the year.

- Final Return: You submit one final VAT return at the end of the year to balance your payments.

Other Special Schemes

There are several other VAT schemes designed to meet the needs of different types of businesses:

- Flat Rate Scheme: This scheme simplifies the process by allowing businesses to pay a fixed percentage of their turnover as VAT. It’s suitable for businesses with a VAT-exclusive turnover of £150,000 or less. You don’t reclaim VAT on purchases, except for certain capital assets over £2,000.

- Cash Accounting Scheme: Under this scheme, you only pay VAT on sales when you receive payment from your customers, and you only reclaim VAT on purchases when you pay your suppliers. This can help with cash flow management, especially for businesses with late-paying customers.