Key takeaways

- Goods exported from the UK to any overseas destination are usually zero-rated for VAT purposes, provided you retain proof of export such as customs declarations or courier tracking.

- B2B services supplied to overseas businesses generally fall outside the scope of UK VAT because the customer accounts for VAT in their own country under the reverse charge mechanism.

- Digital services sold to EU consumers must carry VAT at the customer's country rate, and UK sellers can use the One Stop Shop (OSS) scheme to report and pay it.

- The Import One Stop Shop (IOSS) lets UK sellers collect EU VAT at checkout on goods shipped to EU consumers in parcels valued under EUR 150, avoiding border delays.

- HMRC requires at least two non-conflicting pieces of evidence of customer location for digital sales, such as billing address and bank country, to support the VAT treatment applied.

Selling Outside UK? Here’s What You Need to Know About VAT

VAT - three little letters, endless headaches. It’s the tax you apply to most sales in the UK, and for domestic deals, it’s pretty simple. The real complications start when you begin selling to customers abroad. Many business owners find themselves asking the same question: Do I have to charge VAT to overseas customers?

Honestly, there’s no one-size-fits-all answer. It all depends on a handful of things: Are you selling goods or services? Is your customer a business or just someone buying for themselves? Are they based in the EU, or outside it?

Let’s break it down, so you know exactly when VAT applies, when it doesn’t, and what records you need to keep.

When Do You Need to Charge VAT on Overseas Sales?

If you’re selling within the UK, you’re charging VAT as normally using the standard UK VAT rates, no surprises there. But once your sales cross UK borders, things get a bit more complicated. The main thing to keep in mind is the “place of supply.” That’s what determines which country’s VAT rules you need to follow.

Here’s how it works in practice:

Goods:

The key question is: where are your products when you sell them? If you’re shipping goods overseas, the place of supply is considered outside the UK. In practice, you can usually zero-rate that sale for UK VAT purposes. Your customer on the other end will handle any import VAT in their own country.

Services

The place of supply depends on who your customer is:

- B2B (business-to-business): The place of supply is normally where your customer is based. In most cases, you won’t charge UK VAT, they’ll account for VAT themselves under the reverse charge.

- B2C (business-to-consumer): The place of supply is often where you, the supplier, are based. You may still need to charge UK VAT, unless your service falls under a special category (for example, digital services, which follow different treatment in the EU).

To put it simply, whether you need to charge VAT overseas depends on:

What you sell – goods or services

The rules differ depending on whether you’re selling physical products that are shipped abroad or services that are supplied to customers overseas.

Who you sell to – business or consumer

Sales to overseas businesses (B2B) are usually treated differently from sales to individual consumers (B2C). For example, a business customer in another country may handle VAT on their side, while a consumer might need to be charged UK VAT.

Where your customer is – EU or outside the EU

The location of your customer matters a lot. Selling to the EU often comes with specific VAT schemes and reporting requirements, while sales to countries outside the EU are usually treated as exports and may be zero-rated.

Understanding ‘Place of Supply’

Understanding the concept of 'place of supply' is fundamental to determine your VAT obligations. It refers to the location where your goods or services are considered to be supplied for tax purposes. The rules for determining the 'place of supply' differ for goods and services.

- For Goods: The ‘place of supply’ is the place where you make a supply and where you may be charged and pay VAT.

- For Services: There are various rules to determine the “place of supply” depending on:

- whether you’ve more than one business location

- the kind of service you provide

- the place where your business or your business customer ‘belongs’

When Do Businesses Need to Register for VAT?

In the UK, Value Added Tax (VAT) is a tax collected by businesses registered for VAT and paid to HMRC. If your business's annual turnover exceeds the VAT threshold 2025 i.e £90,000, you are legally required to register for VAT. This VAT threshold includes all the income from UK and EU services, assets, and taxable income. Typically, businesses pass on this tax to their business customers.

Sometimes, businesses choose to register for VAT even when their turnover is below £90,000 so that they can reclaim the VAT paid on their business purchases. Registering for VAT is not possible if your business sells VAT-exempt services or goods.

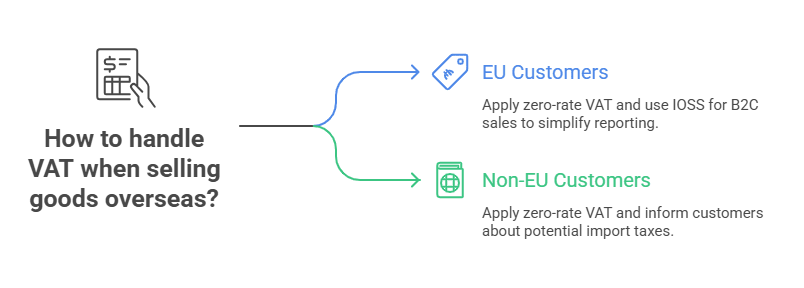

Selling Goods Overseas – VAT Rules

When you sell physical goods abroad, the VAT treatment depends on whether your customer is in the EU or outside it.

To EU Customers (B2B & B2C)

Zero-rated exports

When you export goods from the UK to EU countries, you generally apply zero-rate VAT. But, it’s essential you keep proper records to prove those goods actually left the UK. Otherwise, you could run into compliance headaches.

Import One Stop Shop (IOSS)

If you’re selling directly to EU consumers (B2C), there’s the IOSS system to simplify VAT reporting. So, instead of registering for VAT in every country you sell to, you use IOSS to declare and pay the VAT due in one place. For online sellers shipping multiple small parcels across Europe, this can save a lot of admin time and effort.

To Non-EU Customers

Zero-rated exports

Goods you export to countries outside the EU are also typically zero-rated for UK VAT, provided you can verify that the goods were exported. Again, record keeping is key here.

Import taxes abroad

You don’t add UK VAT, but your customers abroad may still face import VAT, customs duties, or other local taxes when their goods arrive in their country. It’s good practice to inform your customers about these potential charges up front, so there are no surprises when their shipment is delivered.

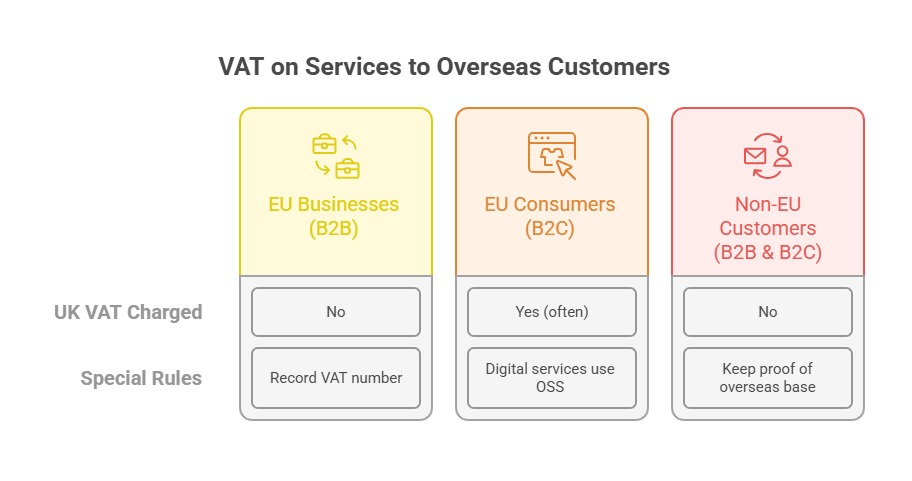

VAT on Services to Overseas Customers

VAT on services don’t follow the same treatment as with goods. The rules purely depend on whether you’re dealing with a business or a consumer, and their location is everything.

To EU Businesses (B2B)

If you provide services to a VAT-registered business in the EU, you usually don’t charge UK VAT. Instead, your client handles their own country’s VAT through the reverse charge mechanism. Make sure you record their VAT number, just in case HMRC asks for proof that they’re a genuine business customer.

To EU Consumers (B2C)

If you sell services directly to individual consumers in the EU, you often need to charge UK VAT as the place of supply is considered the UK. That said, digital services like apps, streaming, downloads, fall under special rules. For those, VAT is due in the customer’s country of residence, and you may need to use the One Stop Shop (OSS) system to report and pay VAT throughout the EU.

To Non-EU Customers (B2B & B2C)

For customers outside the EU, whether businesses or consumers, your services are typically outside the scope of UK VAT. That means there’s no need to add VAT to your invoice. Still, it’s important to keep solid proof showing your customer is based overseas, in case HMRC asks.

VAT on International Sales - at a Glance

Common Scenarios Explained

VAT on overseas sales can sound complicated, so let’s break it down with some everyday examples.

1. “I sell handmade goods to US customers – do I charge VAT?”

If you’re exporting physical products like jewellery or crafts to US customers, you generally don’t charge UK VAT. These are zero-rated exports, provided you keep proof the items left the UK. Be aware, though, your US customers may be liable for any local import VAT or customs duties when the goods arrive.

2. “I provide consultancy to EU businesses – do I charge VAT?”

When your client is a VAT-registered business in the EU, UK VAT doesn’t apply. Instead, the client is responsible for accounting for VAT under the reverse charge mechanism on their end. Always retain their VAT number for your records in case HMRC requests verification.

3. “I sell digital downloads to EU consumers – do I charge VAT?”

Yes, VAT is applied here, though not UK VAT. For digital products (such as eBooks, software, or music) sold to EU consumers, VAT must be charged at the rate in the customer’s country of residence. You’ll need to register for the EU’s OSS (One Stop Shop) scheme to report and pay VAT collected from all relevant EU countries.

4. “I run an online shop shipping worldwide – how do I handle VAT?”

For sales to UK customers, standard UK VAT applies. For customers outside the UK, most sales are zero-rated exports, so you won’t charge UK VAT, but local taxes or customs fees may apply for your customers. If you sell to EU consumers, the IOSS scheme may be needed for parcels under €150, enabling VAT collection at checkout rather than at the border.

Records You Must Keep for Overseas Sales

Dealing with overseas sales? Honestly, solid paperwork is just as vital as knowing your VAT obligations. HMRC can (and will) ask you to prove why you did or didn’t charge VAT. If your records aren’t in order, you’re leaving your business exposed.

Here are the main records you should keep:

Proof of Export (for Goods)

If you’re exporting goods out of the UK, you must be able to show the goods genuinely left the country. This proof could include:

- Commercial invoices

- Shipping company paperwork

- Customs declarations

- Tracking numbers or delivery confirmations

Without proper proof, HMRC might decide your goods never left the UK and hit you with unexpected VAT charges.

Customer VAT Number (for B2B Services)

Selling services to VAT-registered businesses in the EU? You don’t usually charge UK VAT, they handle it with the reverse charge. But you must keep your customer’s valid VAT number and business details on file. That’s your proof they’re a genuine business, not just a private individual.

Evidence of Customer Location (for Digital Products)

For digital sales such as ebooks, software subscriptions, streaming, you’re expected to apply VAT based on where your customer lives. So, you need to gather evidence of their location, such as:

- Billing address

- Bank or card info showing country

- IP address logs

You’ll need at least two non-conflicting pieces of evidence to demonstrate you’ve applied the correct VAT rules.

Sort Your UK VAT on Overseas Sales Today with GoForma

VAT on international sales seems complicated. It really depends on whether you’re dealing with goods or services, who your customer is, and where they’re based. On top of that, schemes like OSS and IOSS add another layer of admin, and HMRC expects everything to be backed up with detailed records - miss something, and you could be looking at penalties.

Because no two businesses are the same, that’s why it’s smart to get advice tailored to your situation. Working with a VAT specialist or small business accountant can help you avoid costly mistakes and bring clarity to your next steps.

A specialist accountant can:

- Help you apply the right rules for each type of sale

- Handle VAT reporting and international schemes such as OSS and IOSS

- Keep your records in order so you avoid HMRC penalties

- Save you time so you can focus on running your business

At GoForma, we support small businesses and contractors with VAT for international sales every day. If you’re looking for expert advice that fits your business, book a free consultation with us before your next overseas sale. You’ll be glad you did.