Introduction

This article is updated regularly as events unfold.

Enough drama and politics, in practical terms, what is actually going to happen?

Accurately predicting the future has never been easy, and the people who claim to know how to do it usually get it wrong - often due to the methodologies they have to work within.

The task gets even more convoluted with a large geopolitical development like Brexit: clear waters are muddied by personal political agendas and few people really understand things like macroeconomics, grand strategy or the development of purpose which fits history together.

We're not going to explain any of that here, where we just focus on the practicalities of the process: those legislative and business factors which are already in position.

The big question is whether Brexit will tank the UK economy. The short answer is no, because of cui bono, or those who stand to benefit.

The little questions are: to what extent will Brexit inconvenience you in your business and personal life? And the answer to that one is 'not much'.

Let's look at the actual structural changes that Brexit will result in as we piece together an apolitical, non-sensationalist picture of what is really going on.

Singapore on Thames

The tax justice network has done an excellent job of thoroughly investigating the potential which Brexit holds for the development of Britain's financial sector.

As they note:

"Senior government ministers have been signalling the Singapore-on-Thames development strategy since January 2017, when Prime Minister May and her Chancellor Philip Hammond both flagged it up as a potential route."

Such a set of arrangements would by no means be easy to negotiate, and even the preliminaries have proven problematic.

A variety of views currently prevail as to the effect of Brexit on the UK's financial sector. Both academic studies and Deutsche bank's CEO do not think that Brexit will diminish the importance of the City of London as a global financial hub.

In every crisis there is also opportunity, and without EU oversight the potential definitely exists for the UK to reinvent itself in much the same way as the USA did with their FATCA legislation. Suggesting that this might well have been the plan from before the start at some level should of course be understood as pure speculation. It will, however, happen.

Current state of play

Immediately following the referendum, it was estimated that 75,000 banking jobs would be moved to the EU, primarily to Paris and Frankfurt. In practice, as the BBC discovered, hundreds of banking jobs have been moved, but hundreds is not thousands.

Bloomberg has compiled an ongoing tracker showing which firms and sectors have so far been affected and how.

According to some estimates, Brexit has already resulted in nearly 500,000 jobs lost in the UK due to downsizing and companies moving overseas.

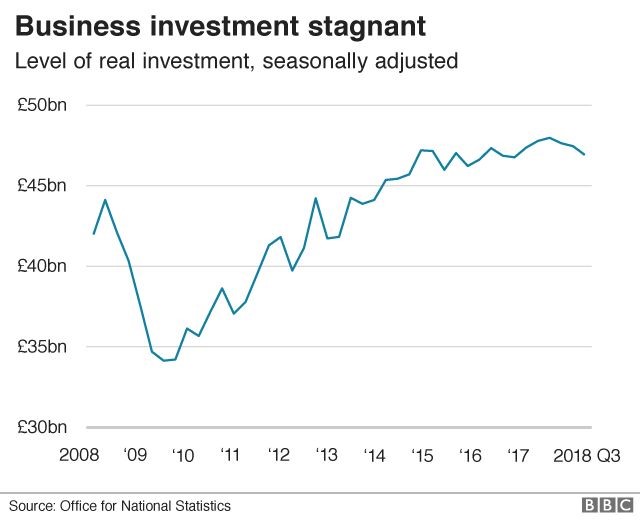

Business investment: no marked downwards trend

Business investment overall has been stagnant since before the referendum:

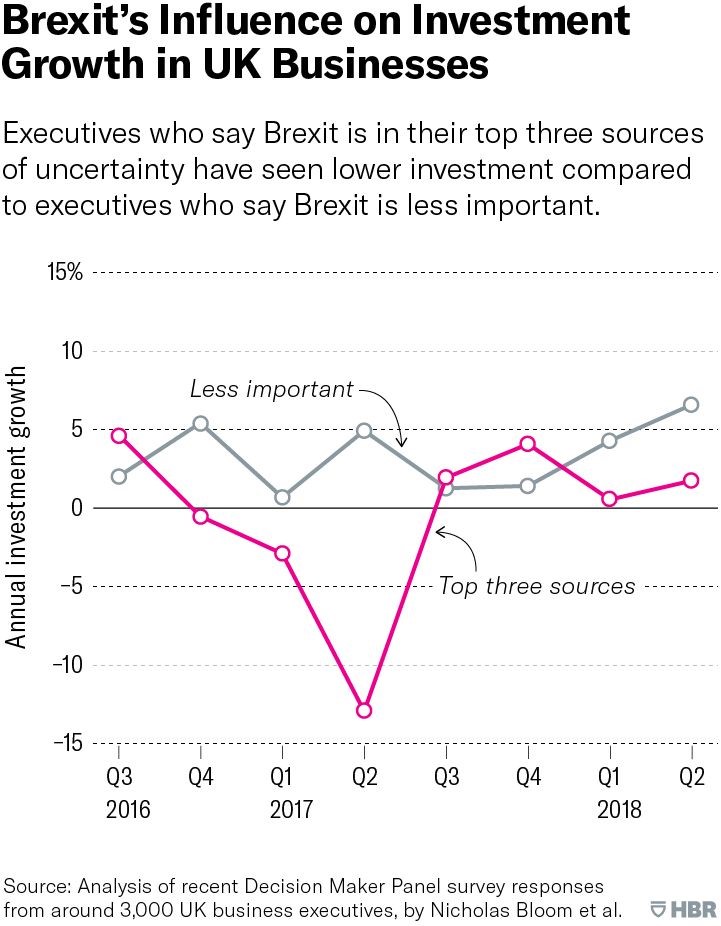

A more detailed analysis by Bloom et al. reveals that Brexit has affected business investment, but it has done so in a statistically significant way only for businesses whose executives regard Brexit as one of the top three sources of uncertainty they are facing:

The majority of the effects in this appear to have been temporary, and due to the more nebulous factor of business confidence rather than hard structural reasons. It is an overextension to say that Brexit itself has already produced a marked departure from trend in business investment.

International trade

In the event of a no deal Brexit, new trade agreements will have to be negotiated by the UK on the basis of WTO and GATT rules. The UK is not permitted to negotiate any such agreements prior to Brexit.

It is estimated that such agreements will take between two to 10 years to negotiate.

In practice, in the short term, it is likely that the UK will continue to trade with the EU states and other countries on the basis of the WTO schedules from when the UK was an EU member.

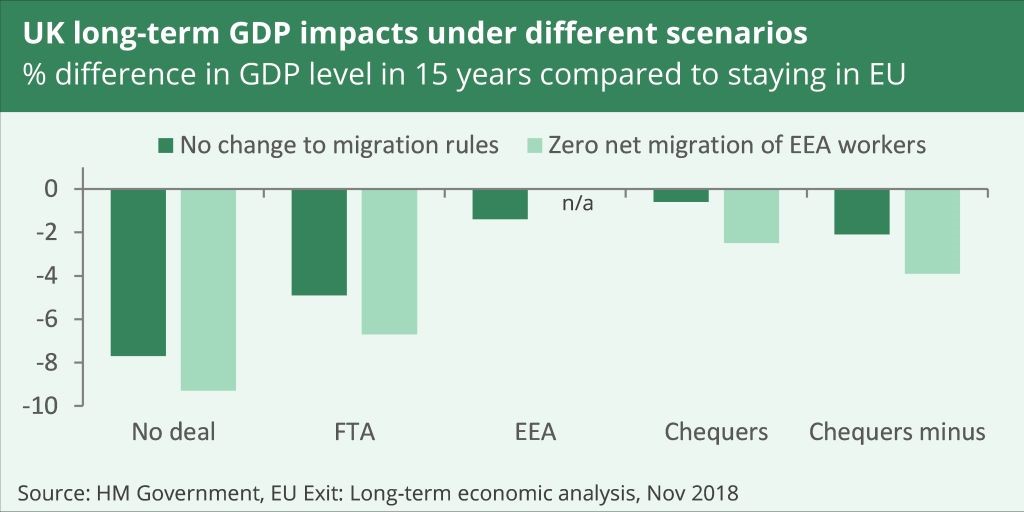

Different scenarios are still in play, and these were the basis for the different GDP projections in the government's 2018 long-term analysis of the British economy:

These effects are likely to be more than offset by the proposals for Singapore on Thames mentioned above which are currently "still being investigated".

Legislative and regulatory context: only tiny changes

The European Union (Withdrawal) Act 2018 aims to incorporate existing EU laws within British domestic legislation, whilst leaving their provisions unchanged.

Only two real changes will be required of British domestic legal structure.

Firstly, the governing or regulatory bodies referred to in the legal structure will have to be replaced by their corresponding domestic counterparts. For example, the European Court of Justice will no longer have jurisdiction over Britain.

Secondly, legislation relating to VAT and import and export duties will have to change as reciprocal agreements may no longer be in place, or will be in place to a lesser extent and according to a different set of conditions.

Business administrative procedure

With a deal or without one, business administration will be affected by Brexit.

Once the UK leaves the EU, EU institutions will have no jurisdiction within the UK. Whilst the majority of EU law has been incorporated into British legal statute, different institutions will be responsible for administering those laws.

Areas which will be affected include:

- European standards

- Intellectual property rights, such as patents, trademarks and copyrights

- Professional qualifications

- Product labelling requirements

If your business is in a field or industry where extensive changes will be required then you have probably already done your own Brexit impact assessment. Should you wish to review this in the light of the latest developments, TechUK has an extensive list of what will be involved in specific industry sectors.

If you currently employ EU nationals in the UK, then you need to ensure they apply for settled or pre-settled status. They will be eligible if they started living here before the UK leaves the EU without a deal, or by December 2020 in the event a deal is agreed.

Tax and VAT

If you currently receive dividends, interest or royalty payments from companies within the EU then post-Brexit you will have to rely on individual tax treaties for relief. The UK does already have these with the EU27 nations, but the precise terms are different in each case.

In the event of a no deal Brexit:

- You will still be able to claim VAT refunds from the EU27 countries, but will have to use the procedures already in place for non-EU businesses.

- The EU VAT refund system would no longer be available. HMRC have said they are developing a parallel system to list UK VAT numbers. UK users would still be able to access the online EU VAT number validation service, but UK VAT numbers will no longer be held within it.

- Goods imported from the EU will be subject to the same rules and tariffs currently imposed on non-EU imports.

- Low Value Consignment Relief (LVCR) will be eradicated on all parcels entering the UK, on which VAT will have to be paid.

HMRC has already made preparations for dealing with VAT in the event of a no deal Brexit.

The net effect

Bar a few administrative hurdles, not much will change overall by the looks of it. There certainly seems to be a lot less reason to panic than ordinary press reports would have you believe.

At Forma, we provide everything you need to get started as a freelancer, contractor or small business owner. If you need business advice or guidance in relation to Brexit outcomes, planning or mitigation strategies please get in touch with us here.